Table of Contents

As filed with the Securities and Exchange Commission on March 20, 2014

Registration No. 333-193798

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Antero Resources Midstream LLC

to be converted as described herein into a limited partnership named

Antero Midstream Partners LP

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

|

| Delaware |

|

4922 |

|

46-4109058 |

(State or Other Jurisdiction of

Incorporation or Organization) |

|

(Primary Standard Industrial

Classification Code Number) |

|

(IRS Employer

Identification Number) |

1625 17th Street

Denver, Colorado 80202

(303) 357-7310

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices) |

Glen C. Warren, Jr.

1625 17th Street

Denver, Colorado 80202

(303) 357-7310

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service) |

Copies to:

|

|

|

David P. Oelman

Matthew R. Pacey

Vinson & Elkins L.L.P.

1001 Fannin, Suite 2500

Houston, Texas 77002

(713) 758-2222 |

|

Ryan J. Maierson

Latham & Watkins LLP

811 Main Street, Suite 3700

Houston, Texas 77002

(713) 546-5400 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If

any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the

following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list

the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities

Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act

registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the

definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

|

|

| Large accelerated filer o |

|

Accelerated filer o |

| Non-accelerated filer ý (Do not check if a smaller reporting company) |

|

Smaller reporting company o |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a

further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the

registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these

securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and we are not

soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated March 20, 2014

PROSPECTUS

Antero Midstream Partners LP

Common Units

Representing Limited Partner Interests

This is the initial public offering of common units representing limited partner interests of Antero Midstream Partners LP. No public

market currently exists for our common units.

We have applied to list our common units on the New York Stock Exchange under the symbol "AM."

We

anticipate that the initial public offering price will be between $ and $ per common unit.

Investing in our common units involves risks. Please read "Risk Factors" beginning on page 21 of this prospectus.

These risks include the following:

- •

- Because all of our revenue currently is, and a substantial majority of our revenue over the long term is expected to be,

derived from Antero Resources Corporation ("Antero"), any development that materially and adversely affects Antero's operations, financial condition or market reputation could have a material and

adverse impact on us.

- •

- We may not generate sufficient cash from operations following the establishment of cash reserves and payment of fees and

expenses, including cost reimbursements to our general partner, to enable us to pay the minimum quarterly distribution to our unitholders.

-

•

- Because of the natural decline in production from existing wells, our success depends, in part, on Antero's ability to

replace declining production and our ability to secure new sources of natural gas from Antero or third parties. Additionally, our fresh water distribution services are directly associated with

Antero's well completion activities and water needs, which are partially driven by horizontal lateral lengths and the number of completion stages per well. Any decrease in volumes of natural gas that

Antero produces, any decrease in the number of wells that Antero completes, or any decrease in the length of the laterals Antero drills, could adversely affect our business and operating results.

-

•

- Antero, our general partner and their respective affiliates, including Antero Investment, which will own our general

partner, have conflicts of interest with us and limited duties to us and our unitholders, and they may favor their own interests to the detriment of us and our other common unitholders.

-

•

- Our partnership agreement replaces our general partner's fiduciary duties to holders of our units with contractual

standards governing its duties.

-

•

- Holders of our common units have limited voting rights and are not entitled to elect our general partner or its directors,

which could reduce the price at which our common units will trade.

-

•

- You will experience immediate dilution in tangible net book value of $ per common unit.

-

•

- There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may

not develop. The price of our common units may fluctuate significantly, which could cause you to lose all or part of your investment.

- •

- Our tax treatment depends on our status as a partnership for federal income tax purposes, as well as us not being subject

to a material amount of entity-level taxation. If the IRS were to treat us as a corporation for federal income tax purposes, or if we become subject to entity-level taxation for state tax purposes,

our cash available for distribution to you would be substantially reduced.

|

|

|

|

|

|

|

|

|

Per

Common Unit |

|

Total |

Offering price to the public |

|

$ |

|

|

$ |

|

Underwriting discounts and commissions |

|

$ |

|

|

$ |

|

Proceeds to us (before expenses)(1) |

|

$ |

|

|

$ |

|

- (1)

- Excludes

an aggregate structuring fee of % of the gross offering proceeds payable to Barclays Capital Inc. and Citigroup

Global Markets Inc. Please read "Underwriting."

We

have granted the underwriters the option to purchase additional common units on the same terms and conditions set forth above if the underwriters sell more

than

common units in this offering.

Neither

the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities. Any representation to the contrary is a criminal offense.

The

underwriters expect to deliver the common units on or about , 2014.

|

|

|

|

|

| Barclays |

|

Citigroup |

|

Wells Fargo Securities |

Prospectus

dated , 2014

Table of Contents

TABLE OF CONTENTS

i

Table of Contents

ii

Table of Contents

iii

Table of Contents

You

should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on behalf of us or to which we have referred you. We have not

authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus. We take no responsibility for, and can provide no assurance as to

the reliability of, any other information that others may give you. We are offering to sell common units and seeking offers to buy common units only in jurisdictions where offers and sales are

permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the common units. Our business,

financial condition, results of operations and prospects may have changed since that date.

This

prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. Please read "Risk Factors" and

"Cautionary Statement Regarding Forward-Looking Statements."

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry

publications, government publications and other published independent sources. Some data is also based on our good faith estimates. The industry in which we operate is

iv

Table of Contents

subject

to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled "Risk Factors." These and other factors could cause results to differ

materially from those expressed in these publications.

Reserve Information

The estimates of Antero's net proved, probable and possible reserves as of December 31, 2013 included in this prospectus are

based on evaluations prepared by Antero's internal reserve engineers, which have been audited by Antero's independent reserve engineers, DeGolyer and MacNaughton, using SEC pricing and assuming ethane

rejection.

Certain Terms Used in this Prospectus

All references in this prospectus to:

- •

- "we," "our," "us" or like terms when used in the present tense or prospectively refer to Antero Midstream

Partners LP and its subsidiaries;

- •

- "Predecessor," "we," "our," "us" or like terms when used in a historical context refer to Antero's midstream business and

assets to be contributed to Midstream Operating prior to the closing of this offering;

- •

- "Midstream Operating" refer to Antero Resources Midstream Operating LLC, which will own Antero's midstream business

and assets at the closing of this offering, at which point Midstream Operating will be contributed to us;

- •

- "Antero" refer to Antero Resources Corporation;

- •

- "Antero Investment" refer to Antero Resources Investment LLC, the owner of our general partner;

- •

- "our general partner" or "Midstream Management" refer to Antero Resources Midstream Management LLC;

- •

- "our employees" refer to the employees of Antero that will conduct our business;

- •

- "Sponsors" refer to Warburg Pincus LLC, Yorktown Partners LLC and Trilantic Capital Partners;

- •

- "excluded acreage" refer to Antero's existing acreage not dedicated to us for gathering and compression services,

consisting of 128,000 net leasehold acres dedicated to third-party gatherers as described in "Business—Antero's Existing Third-Party Commitments—Excluded Acreage"; and

- •

- "existing third-party commitments" refer to Antero's existing minimum volume commitments to parties other than us, as

described in "Business—Antero's Existing Third-Party Commitments—Other Commitments," together with the excluded acreage.

v

Table of Contents

SUMMARY

This summary provides a brief overview of information contained elsewhere in this prospectus. You should read

this entire prospectus and the documents to which we refer you before making an investment decision. You should carefully consider the information set forth under "Risk Factors," "Cautionary Statement

Regarding Forward-Looking Statements" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" as well as the historical financial statements and the related notes

to those financial statements included elsewhere in this prospectus and the

pro forma financial statements and related notes to those financial statements included elsewhere in this prospectus. The information presented in this prospectus assumes an initial public offering

price of $ per common unit (the mid-point of the price range set forth on the cover page of this prospectus) and, unless otherwise indicated, that the underwriters' option to

purchase

additional common units is not exercised.

We include a glossary of some of the terms used in this prospectus as Appendix B.

Antero Midstream Partners LP

Overview

We are a growth-oriented limited partnership formed by Antero Resources Corporation (NYSE: AR) to own, operate and develop midstream

energy assets to service Antero's rapidly increasing production. Our assets consist of gathering pipelines, compressor stations and fresh water distribution systems, through which we provide midstream

services to Antero under long-term, fixed-fee contracts. Our assets are located in the rapidly developing liquids-rich southwestern core of the Marcellus Shale in northwest West Virginia and

liquids-rich core of the Utica Shale in southern Ohio, which Antero believes are two of the premier North American shale plays. We believe that our strategically located assets and our relationship

with Antero position us to become a leading midstream energy company serving the Marcellus and Utica Shales.

Pursuant to our long-term contracts with Antero, we have secured 20-year dedications covering (i) substantially all of Antero's current and future acreage for gathering and

compression services and (ii) all of Antero's current and future acreage for fresh water distribution for well completion operations. All of Antero's existing acreage is dedicated to us for

gathering and compression services except for the existing third-party commitments, which includes 128,000 Marcellus Shale net leasehold acres characterized by dry gas and liquids-rich

production that have been previously dedicated to third-party gatherers. Please read "Business—Antero's Existing Third-Party Commitments." Net of the excluded acreage, our contracts cover

approximately 329,000 net leasehold acres held by Antero as of February 28, 2014 for gathering and compression services and all 457,000 of Antero's existing net leasehold acres for fresh water

distribution services. In addition to Antero's existing acreage dedication, our agreements provide that any acreage Antero acquires in the future will be dedicated to us for gathering and compression

and fresh water distribution services.

In

the future, we may also provide condensate gathering services to Antero under the gathering and compression agreement. We also have entered into a right-of-first-offer agreement with

Antero to allow for us to provide Antero with natural gas processing services in the future. As a result of Antero's acreage dedication and its contribution to us of substantially all of its midstream

assets in connection with this offering, we believe that we possess significant organic growth potential and, unlike many other midstream companies, our growth does not depend on future acquisitions

of assets from our sponsor or third parties.

Antero

is our only customer and is one of the largest producers of natural gas and NGLs in the Appalachian Basin. As of December 31, 2013, Antero's estimated net proved, probable

and possible reserves were 7.6 Tcfe, 19.8 Tcfe and 7.5 Tcfe, respectively, of which 85% was natural gas. As of December 31, 2013, Antero's drilling inventory consisted of 4,778 identified

potential horizontal well

1

Table of Contents

locations (2,978 of which were located on acreage dedicated to us) for gathering and compression services, which provides us with significant opportunity for growth as Antero's robust drilling program

continues and its production increases. Based on information from RigData, Antero is currently the most active driller in the Appalachian Basin with 20 operated rigs, including 15 operated rigs in the

Marcellus Shale (where it is the most active driller) and 5 operated rigs in the Utica Shale (where it is one of the most active drillers). On January 29, 2014, Antero announced a 2014 drilling

and completion capital expenditures budget of approximately $1.8 billion that provides for the drilling of approximately 193 wells, a substantial increase over the 157 wells drilled in 2013.

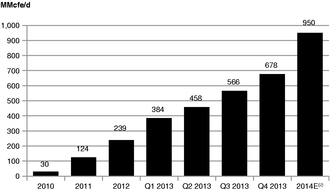

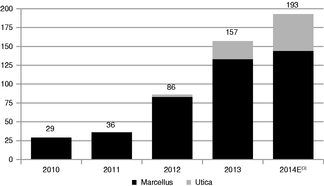

Antero's average Appalachian production during 2013 represented an increase of 115% as compared to 2012, and its net production in the fourth quarter of 2013 averaged 678 MMcfe/d. We anticipate that

Antero's robust drilling program will significantly increase throughput on our gathering and compression systems and will result in a significant demand for our fresh water distribution services.

The

charts below illustrate the significant Appalachian Basin production growth achieved by Antero since the acquisition of its Marcellus Shale leasehold in 2008 and the growth in wells

drilled as it has undertaken its development program. We believe that Antero will rely on us to deliver the midstream infrastructure necessary to support its continued growth, which should result in

significant increases in our gathering and compression and fresh water distribution volumes.

|

|

|

| Antero's Average Net Daily Production(1) |

|

Antero's Operated Gross Wells Spud(1) |

|

|

|

- (1)

- Represents

all of Antero's Appalachian Basin production and wells drilled for the periods indicated, including production from wells drilled

on the excluded acreage. For a discussion of the anticipated throughput of our gathering and compression systems, please read "Our Cash Distribution Policy and Restrictions on

Distributions—Assumptions and Considerations—Results, Volumes and Fees."

- (2)

- Represents

the mid-point of Antero's anticipated average net daily production for the year ending December 31, 2014 of between 925 and

975 MMcfe/d.

- (3)

- Represents

Antero's estimate of the number of wells it intends to spud in 2014.

The following table highlights the scale of Antero's net acreage position and gross drilling locations dedicated to us as of December 31, 2013. With 4,778 identified potential

horizontal well locations included in Antero's net proved, probable and possible reserves as of December 31, 2013, Antero

2

Table of Contents

maintains

a 24-year drilling inventory (based on expected 2014 drilling activity), which we believe will provide significant demand for further gathering and compression and fresh water distribution

services.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Drilling Locations |

|

2014

Estimated

Completion

Activity |

|

|

|

Net

Acres |

|

Dry

Gas |

|

Rich

Gas |

|

Highly

Rich Gas |

|

Highly

Rich Gas/

Condensate |

|

Total |

|

Average

Rigs |

|

Wells |

|

Gathering and Compression: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Marcellus Gathering and Compression |

|

|

220,000 |

|

|

340 |

|

|

374 |

|

|

861 |

|

|

644 |

|

|

2,219 |

(1) |

|

9 |

|

|

72 |

|

Utica Gathering and Compression |

|

|

106,000 |

|

|

211 |

|

|

182 |

|

|

161 |

|

|

205 |

|

|

759 |

|

|

4 |

|

|

41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Gathering and Compression Dedicated to Us(2) |

|

|

326,000 |

|

|

551 |

|

|

556 |

|

|

1,022 |

|

|

849 |

|

|

2,978 |

|

|

13 |

|

|

113 |

|

Excluded acreage(3) |

|

|

128,000 |

|

|

957 |

|

|

811 |

|

|

32 |

|

|

— |

|

|

1,800 |

|

|

5 |

|

|

68 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

454,000 |

|

|

1,508 |

|

|

1,367 |

|

|

1,054 |

|

|

849 |

|

|

4,778 |

|

|

18 |

|

|

181 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fresh Water Distribution: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Marcellus |

|

|

348,000 |

|

|

1,297 |

|

|

1,185 |

|

|

893 |

|

|

644 |

|

|

4,019 |

|

|

14 |

|

|

126 |

|

Utica |

|

|

106,000 |

|

|

211 |

|

|

182 |

|

|

161 |

|

|

205 |

|

|

759 |

|

|

4 |

|

|

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

454,000 |

|

|

1,508 |

|

|

1,367 |

|

|

1,054 |

|

|

849 |

|

|

4,778 |

|

|

18 |

|

|

163 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- (1)

- Includes

Upper Devonian locations not expected to be drilled during the twelve-month period ending March 31, 2015. See "Our Cash

Distribution Policy and Restrictions on Distributions—Estimated Cash Available for Distribution for the Twelve-Months Ending March 31, 2015."

- (2)

- Antero's

estimated net proved, probable and possible reserves associated with this acreage were 3.1 Tcfe, 15.3 Tcfe and

4.6 Tcfe, respectively, as of December 31, 2013. See "Business—Antero's Existing Third-Party Commitments."

- (3)

- The

excluded acreage is associated with approximately 4.5 Tcfe, 4.5 Tcfe and 2.9 Tcfe of Antero's net proved, probable and possible reserves,

respectively, as of December 31, 2013.

Antero's core operating areas are located in liquids-rich portions of the Marcellus and Utica Shales, which Antero believes are two of North America's premier shale plays. The Marcellus

Shale is characterized by consistent and predictable geology, high well recoveries relative to drilling and completion costs and significant hydrocarbon resources in place. Based on these attributes,

as well as Antero's drilling results and those publicly released by other operators, Antero believes that the Marcellus Shale offers some of the most attractive single-well rates of return of all

North American conventional and unconventional play types. Antero believes that the Marcellus Shale has two core areas: the southwestern core in northern West Virginia and southwestern Pennsylvania

and the northeastern core in northeastern Pennsylvania. All of Antero's approximately 351,000 net leasehold acres in the Marcellus Shale are located within the southwestern core, where it has

experienced virtually no geologic complexity in its drilling activities to date. According to RigData, as of February 28, 2014, approximately 90% of the 94 drilling rigs operating in the

Marcellus Shale were located in these two core areas.

Based on drilling results and initial production from Antero's 16 core area Utica Shale wells, Antero believes that the Utica Shale also offers some of the most attractive single-well

rates of return of all North American conventional and unconventional plays. Antero believes that the core area is located in the southern portion of the play, where the majority of the most

productive Utica Shale wells are located. Antero owns approximately 106,000 net leasehold acres in the core of the Utica Shale and expects to continue to add to its sizeable land position.

3

Table of Contents

We believe that Antero's large portfolio of repeatable, low cost, liquids-rich drilling opportunities in the Marcellus and Utica Shales supports strong well

economics in a variety of commodity price environments. As a result, we expect strong and growing demand for our gathering and compression and fresh water distribution services as the number of

Antero's well completions and throughput volumes increase.

In

addition to the growth we anticipate as a result of Antero's development drilling, we believe we will be able to attract third-party customers as other upstream operators in the

Marcellus and Utica Shales

require infrastructure to move their product to market and ensure distribution of fresh water for their well completions.

Our Contractual Arrangements with Antero

We believe that Antero's acreage dedication to us, robust drilling program and expected production growth, combined with our fixed-fee,

life of reserves business model, provide us with significant growth opportunities.

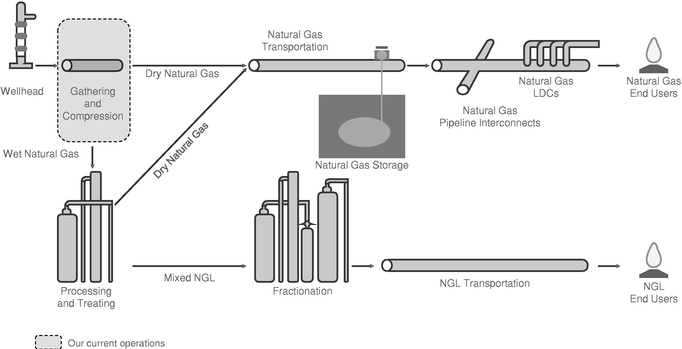

Gathering and Compression

Pursuant to our 20-year gathering and compression agreement, Antero has agreed to dedicate all of its current and future acreage in

West Virginia, Ohio and Pennsylvania to us (other than the existing third-party commitments). For a discussion of Antero's existing third-party commitments, please read "Business—Antero's

Existing Third-Party Commitments." We also have an option to gather and compress natural gas produced by Antero on any acreage it acquires in the future outside of West Virginia, Ohio and Pennsylvania

on the same terms and conditions. Under the gathering and compression agreement, we receive a low-pressure gathering fee of $0.30 per Mcf, a high-pressure gathering fee of $0.18 per Mcf and a

compression fee of $0.18 per Mcf. Any handling and treating of condensate will be priced on a cost of services basis. If and to the extent Antero requests that we construct new high-pressure lines and

compressor stations, the gathering and compression agreement contains minimum volume commitments that require Antero to utilize or pay for 75% and 70%, respectively, of the capacity of such new

construction. Additional high-pressure lines and compressor stations installed on our own initiative are not subject to such volume commitments. These minimum volume commitments on new infrastructure

are intended to support the stability of our cash flows.

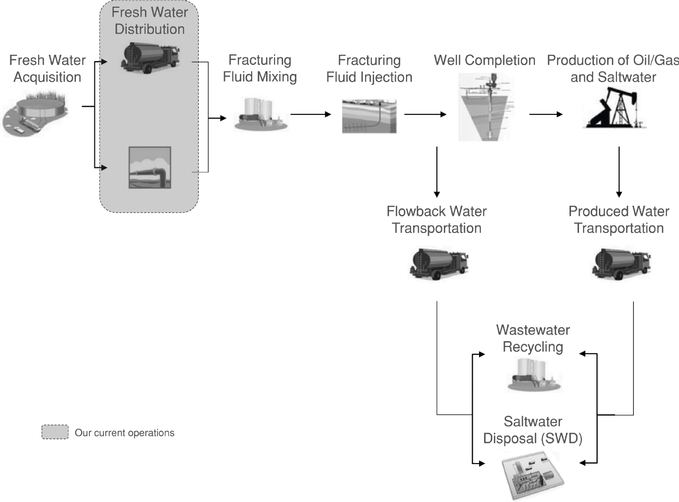

Fresh Water Distribution

In addition to the gathering and compression agreement, we have also entered into a 20-year fresh water distribution agreement with

Antero, pursuant to which a service area encompassing all of Antero's areas of operation in West Virginia, Ohio and Pennsylvania is dedicated to us. If Antero requires fresh water distribution

services outside of the initial service area, we will have the option to provide those services on the same terms and conditions. Under the fresh water

distribution agreement, we will receive a fee of $3.50 per barrel for fresh water deliveries by pipeline to well sites or $3.00 per barrel if Antero accesses the water by truck directly from our

storage facilities.

Processing

Although we do not currently have any processing or NGL fractionation, transportation or marketing infrastructure, we have entered into

a right-of-first-offer agreement with Antero for gas processing services, pursuant to which Antero has agreed, subject to certain exceptions, not to procure any gas processing or NGL fractionation,

transportation or marketing services with respect to its production (other than production subject to a pre-existing dedication) without first offering us the right to provide such services. For a

discussion of Antero's existing third-party commitments, please read "Business—Antero's Existing Third-Party Commitments."

4

Table of Contents

Our Existing Assets and Growth Projects

In connection with the completion of this offering, Antero will contribute substantially all of its midstream assets to us, as well as

the right to develop additional midstream infrastructure to service Antero's rapidly growing production. Because of our close operational and contractual relationship with Antero, we expect to grow

significantly as Antero pursues its development plan.

Gathering and Compression

The following table provides information regarding our gathering and compression system as of December 31, 2013 and operations

for the fourth quarter of 2013, as well as our expectations for organic growth in these assets as of December 31, 2014, based on Antero's drilling and completion plans.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Low-Pressure

Pipeline

(miles) |

|

High-Pressure

Pipeline

(miles) |

|

Oil

Pipeline

(miles) |

|

Compression

Capacity

(MMcf/d) |

|

|

|

|

|

Average Daily

Throughput for the

Three Months Ended

December 31, 2013

(MMcf/d) |

|

|

|

As of December 31, |

|

|

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

Gathering and Compression System: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Marcellus |

|

|

54 |

|

|

125 |

|

|

38 |

|

|

67 |

|

|

— |

|

|

— |

|

|

105 |

|

|

410 |

|

|

232 |

|

Utica |

|

|

26 |

|

|

55 |

|

|

23 |

|

|

37 |

|

|

10 |

|

|

20 |

|

|

— |

|

|

120 |

|

|

61 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

80 |

|

|

180 |

|

|

61 |

|

|

104 |

|

|

10 |

|

|

20 |

|

|

105 |

|

|

530 |

|

|

293 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Our

midstream infrastructure includes a network of 8-, 12-, 16- and 20-inch gathering pipelines and compressor stations that collects raw natural gas from Antero's operations in the

Marcellus and Utica Shales. Our compression assets currently only service Antero's operations in the Marcellus Shale area, but we may expand our compression capacity to service the Utica Shale area in

2014.

In 2014, we anticipate expanding our Marcellus and Utica Shale gathering systems to 192 miles and 92 miles, respectively, and growing our year-end daily Marcellus and Utica

compression capacity to 410 MMcf/d and 120MMcf/d, respectively.

Fresh Water Distribution

The following table provides information regarding our fresh water distribution systems as of December 31, 2013 and our

expectations for these assets through December 31, 2014, based on organic growth driven by Antero's drilling and completion plans as announced on January 29, 2014.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Wells

Serviced |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pipeline

(miles) |

|

Fresh Water

Storage

Impoundments |

|

Water Storage

Capacity (MBbl) |

|

|

|

For the year

ended

December 31, |

|

|

|

As of December 31, |

|

|

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

2013 |

|

2014E |

|

Water Distribution Systems: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Marcellus |

|

|

50 |

|

|

126 |

|

|

74 |

|

|

122 |

|

|

14 |

|

|

31 |

|

|

1,475 |

|

|

3,266 |

|

Utica |

|

|

17 |

|

|

37 |

|

|

23 |

|

|

48 |

|

|

7 |

|

|

16 |

|

|

925 |

|

|

3,501 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

67 |

|

|

163 |

|

|

97 |

|

|

170 |

|

|

21 |

|

|

47 |

|

|

2,400 |

|

|

6,767 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Our

midstream infrastructure also includes two independent fresh water distribution systems that distribute fresh water from the Ohio River and several other regional water sources for

producers' well completion operations in the Marcellus and Utica Shales. These systems consist of a combination of permanent buried pipelines, portable surface pipelines and fresh water storage

facilities, as well as pumping stations to transport the fresh water throughout the pipeline networks. To the extent

5

Table of Contents

necessary,

we will move surface pipelines to service completion operations in concert with Antero's robust drilling program. While our fresh water distribution agreement only requires us to distribute

35 barrels of fresh water per minute, our system is capable of distributing approximately 80 barrels of fresh water per minute.

Because hydraulic fracturing depends on substantial volumes of fresh water, our fresh water distribution services will be in greatest demand in connection with completion activities

rather than ongoing well

production. For example, for a typical Antero well that includes a 7,000 foot horizontal lateral and shorter stage lengths, we expect our fresh water distribution services will generate between

$650,000 and $700,000 of revenue for each well Antero completes using water delivered through our system. In addition, we believe that our ability to transport fresh water from the Ohio River, which

is considered reliable in comparison to other water sources in our areas of operation, coupled with our substantial capacity of fresh water impoundments, should enable us to distribute fresh water for

Antero's robust drilling program without material interruption as a result of rainfall variations or other restrictions. We anticipate that approximately 90% of Antero's 2014 well completions will

utilize our fresh water distribution systems.

In

2014, we anticipate expanding our fresh water distribution systems and expect to have 122 and 48 miles of buried water pipelines in the Marcellus and Utica operating areas,

respectively.

Business Strategies

Our principal business objective is to increase the quarterly cash distributions that we pay to our unitholders over time while

ensuring the ongoing stability of our business. We expect to achieve this objective through the following business strategies:

- •

- Leveraging our extensive asset base to meet Antero's current and future infrastructure

needs. We own and operate a high-capacity asset base that we have recently constructed that will allow us to gather and compress

significant incremental natural gas volumes and provide fresh water distribution services for Antero's robust and growing drilling program. We intend to continue to develop our midstream

infrastructure to move Antero's production to market and distribute fresh water for its well completions. In the short-term, we anticipate significant growth in demand for our gathering and

compression and fresh water distribution services driven by Antero's plan to complete approximately 181 horizontal wells in 2014 with an average lateral length of 7,500 feet. In addition, as of

December 31, 2013, Antero's drilling inventory consisted of 4,778 identified potential horizontal well locations (2,978 of which were located on acreage dedicated to us) for gathering and

compression services, giving Antero a 24-year drilling inventory (based on expected 2014 drilling activity) and, consequently, visible long-term demand for our services.

- •

- Focusing on stable, fixed-fee business to avoid direct commodity price

exposure. The gathering and compression and fresh water distribution agreements with Antero provide for fixed-fee structures, and we

intend to continue to pursue additional fixed-fee opportunities with Antero and third parties in order to avoid direct commodity price exposure. We will focus on obtaining additional long-term

commitments from customers, which may include reservation-based charges, volume commitments and acreage dedications.

- •

- Attracting third-party customers. While we will devote

substantially all of our resources to meeting Antero's needs in the near term, we expect to market our services to, and pursue strategic relationships with, third-party producers over time. We believe

that our early, significant footprint of gathering and compression and fresh water distribution systems in the Marcellus and Utica Shales provides us with a competitive advantage that we believe will

allow us to attract third-party natural gas and fresh water volumes in the future.

6

Table of Contents

Competitive Strengths

We believe we are well-positioned to successfully execute our business strategies because of the following competitive

strengths:

- •

- Economic strength of Antero's development program. We

believe the attractiveness of Antero's liquids-rich portfolio of acreage and its low development cost relative to recoveries will support long-term demand for our gathering and compression and fresh

water distribution services in a variety of commodity price environments. The economic strength of Antero's development program is substantially supported by:

- •

- Antero's position in the core of the Marcellus and Utica

Shales. Antero owns and operates extensive and contiguous land positions in the core areas of two of the most economically attractive

North American shale plays, which Antero believes are characterized by consistent geology and high well recoveries relative to drilling and completion costs.

- •

- Antero's multi-year, low-risk drilling inventory. Antero's

drilling inventory at December 31, 2013 consisted of 4,778 identified potential horizontal well locations (2,978 of which were located on acreage dedicated to us) that will require gathering

and compression services. Based on its expected 2014 drilling activity, these locations give Antero a 24-year drilling inventory.

- •

- Antero's exposure to a large resource of liquids-rich gas and

condensate. Liquids-rich gas production generally enhances well economics due to the processing margin generated by higher-value NGL

products, such as propane and butane. In addition, the condensate often associated with liquids-rich production can further increase well economics. Approximately 68% of Antero's 4,778 identified

potential horizontal well locations as of December 31, 2013 target the liquids-rich gas regions of the Marcellus and Utica Shales.

- •

- Antero's status as a low-cost leader. Antero has

implemented operational efficiencies to give it some of the lowest development costs per Mcfe in the Marcellus and Utica Shales, such as (i) drilling longer laterals, (ii) pad drilling,

(iii) the use of shorter stage lengths, (iv) the use of less expensive, shallow vertical drilling rigs to drill to the kick-off point of the horizontal wellbore, (v) the use of

natural gas powered rigs and (vi) the use of our fresh water distribution systems.

-

•

- Antero's access to committed processing and firm takeaway capacity in the Marcellus and Utica

Shales. We believe Antero's existing contractual commitments for processing and firm long-haul transportation help minimize disruptions

to its drilling program that might otherwise exist as a result of insufficient outlets for growing production. Antero has contracted for a total of 950 MMcf/d of processing capacity in the Marcellus

Shale, 550 MMcf/d of which is currently in service. Similarly, Antero has 600 MMcf/d of contracted processing capacity in the Utica Shale, of which 200 MMcf/d is currently in service, with the option

to access 50 MMcf/d of additional capacity. Antero also has secured 1,657,000 MMBtu/d of long-haul firm transportation capacity or firm sales and has committed to 20,000 Bbl/d of ethane takeaway

capacity. We believe our midstream infrastructure, together with Antero's significant processing and takeaway capacity, will allow Antero to commercialize its production more quickly at optimal prices

and keep pace with its robust drilling plan.

- •

- Antero's active hedging program. Antero maintains an

active hedging program designed to mitigate volatility in commodity prices and regional basis differentials and to protect its expected future cash flows. As of December 31, 2013, Antero had

entered into hedging contracts through December 31, 2019 covering a total of approximately 1.3 Tcfe of its projected natural gas and oil production at average index prices of $4.64/MMBtu and

7

Table of Contents

-

•

- Extensive dedication, system scale and long-term, fixed fee contracts to support stable cash

flows. Pursuant to our long-term contracts with Antero, we have secured 20-year dedications covering approximately 329,000 net leasehold

acres held by Antero as of February 28, 2014 (net of the approximately 128,000 excluded net leasehold acres) for gathering and compression services and all 457,000 of Antero's existing net

leasehold acres for fresh water distribution services. Please read "Business—Antero's Existing Third-Party Commitments." In addition to Antero's existing acreage dedication, our agreements

provide that any acreage Antero acquires in the future will be dedicated to us for gathering and compression and fresh water distribution services. We believe that Antero's drilling activity will

result in significant growth of our midstream operations. Our fixed-fee, long-term contract structure eliminates our direct exposure to commodity price risk and provides us with long-term cash flow

stability.

- •

- Financial flexibility and strong capital structure. At the

closing of this offering, we expect to have no outstanding indebtedness and available borrowing capacity of $ million under a new

$ million revolving credit

facility. We believe that our borrowing capacity and our expected ability to effectively access debt and equity capital markets provide us with the financial flexibility necessary to execute our

business strategy.

- •

- Experienced and incentivized management team. Antero's

officers, who will also manage our business, have an average of over 30 years of industry experience and have successfully built, grown and sold two unconventional resource-focused upstream

companies and one midstream company in the past 15 years. We believe Antero's experience and expertise from both an upstream and midstream perspective provides a distinct competitive advantage.

Through our management's ownership interests in Antero Investment, which owns our incentive distribution rights, and their indirect ownership interests in Antero, which will

own of our

common units and all of our subordinated units, our management team is highly incentivized to grow our distributions and the value of our business.

Our Relationship with Antero and Antero Investment

One of our principal strengths is our relationship with Antero. We believe Antero's interests are aligned with ours because Antero

relies on our ability to develop infrastructure in tandem with its drilling and production activities. Upon completion of this offering, Antero will

own common units and

subordinated units in us. Antero's interests are further aligned with ours in that the value of its

retained common and subordinated units should increase to the extent we are

successful in growing our operations. However, as a result of many of the risks associated with Antero's business, we cannot ensure that we will ultimately realize any benefit from our relationship

with Antero. Please read "Risk Factors—Risks Related to Our Business."

In

addition to the alignment of Antero's interests with ours, Antero Investment, which includes members of our and Antero's management and the Sponsors, will own our general partner,

which will own all of the incentive distribution rights. The value of the incentive distribution rights is driven by growth in our distributions. As a result, Antero Investment, including its

management members, are additionally incentivized to facilitate our growth.

Although

our relationship with Antero and Antero Investment provides us with a significant advantage in the midstream market, it also provides a source of potential conflicts. Antero

Investment will own our general partner, which provides Antero Investment with control of our business and may allow Antero Investment to operate our business in a manner inconsistent with the

interests of our unitholders. In addition, Antero Investment will have the right to receive an increasing percentage of our quarterly cash distributions in excess of specified target distribution

levels.

8

Table of Contents

Our Management

Our general partner has sole responsibility for conducting our business and for managing our operations and will be controlled by

Antero Investment. Pursuant to the services agreement that we will enter into concurrently with the closing of this offering, our general partner and Antero will be entitled to reimbursement for all

direct and indirect expenses that they incur on our behalf. Please read "Management's Discussion and Analysis of Financial Condition and Results of Operations—Principal Components of Our

Cost Structure—General and Administrative Expenses" and "Certain Relationships and Related Transactions—Agreements with Affiliates in Connection with the

Transactions—Services Agreement."

Neither

our general partner nor its board of directors will be elected by our unitholders. Antero Investment is the sole member of our general partner and will have the right to appoint

our general partner's entire board of directors. All of our officers and certain of our directors are also officers and directors of Antero.

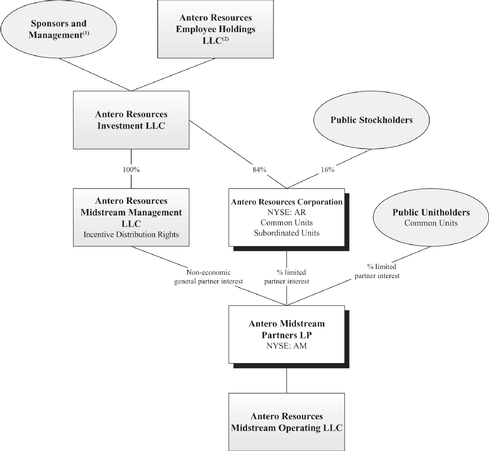

Partnership Structure

In connection with the closing of this offering, Antero will contribute Midstream Operating to us. In connection with that

contribution, we will convert from a limited liability company to a limited partnership, Antero Midstream Partners LP. The diagram below illustrates our organizational structure and ownership

based on total units outstanding after giving effect to the offering and the related transactions and assumes that the underwriters' option to purchase additional common units is not exercised.

|

|

|

|

|

Common Units held by the public |

|

|

|

% |

Common Units held by Antero |

|

|

|

% |

Subordinated Units held by Antero |

|

|

|

% |

General Partner Interest |

|

|

|

* |

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- *

- General

partner interest is non-economic.

9

Table of Contents

- (1)

- Includes

each of our Sponsors and certain members of our management team who have made investments in Antero Investment in exchange for

investment units.

- (2)

- Holds

profits interests in Antero Investment on behalf of members of our management team and other employees. All of the membership interests

in Antero Resources Employee Holdings LLC are held by employees of Antero. The compensation committee of Antero Investment has voting and control rights over the shares held by Antero Resources

Employee Holdings LLC.

10

Table of Contents

Emerging Growth Company Status

We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we are an

"emerging growth company," unlike other public companies, we will not be required to:

- •

- provide an auditor's attestation report on management's assessment of the effectiveness of our system of internal control

over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002;

- •

- comply with any new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB, requiring

mandatory audit firm rotation or a supplement to the auditor's report in which the auditor would be required to provide additional information about the audit and the financial statements of the

issuer;

- •

- comply with any new audit rules adopted by the PCAOB after April 5, 2012, unless the Securities and Exchange

Commission, or the SEC, determines otherwise;

- •

- provide certain disclosure regarding executive compensation required of larger public companies; or

- •

- obtain unitholder approval of any golden parachute payments not previously approved.

We

will cease to be an "emerging growth company" upon the earliest of:

- •

- the last day of the fiscal year in which we have $1.0 billion or more in annual revenues;

- •

- the date on which we become a large accelerated filer;

- •

- the date on which we issue more than $1.0 billion of non-convertible debt over a three-year period; or

- •

- the last day of the fiscal year following the fifth anniversary of our initial public offering.

In

addition, Section 107 of the JOBS Act provides that an "emerging growth company" can take advantage of the extended transition period provided in Section 7(a)(2)(B) of

the Securities Act for complying with new or revised accounting standards, but we intend to irrevocably opt out of the extended transition period.

Risk Factors

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of

our common units. Because of our relationship with Antero, adverse developments or announcements concerning Antero could materially adversely affect our business.

Below is a summary of certain key risk factors that you should consider in evaluating an investment in our common units. However, this list is not exhaustive. Please read the full

discussion of these risks and the other risks described under "Risk Factors" and "Cautionary Statement Regarding Forward-Looking Statements."

Risks Related to Our Business

- •

- Because all of our revenue currently is, and a substantial majority of our revenue over the long term is expected to be,

derived from Antero, any development that materially and adversely affects Antero's operations, financial condition or market reputation could have a material and adverse impact on us.

11

Table of Contents

- •

- We may not generate sufficient cash from operations following the establishment of cash reserves and payment of fees and

expenses, including cost reimbursements to our general partner, to enable us to pay the minimum quarterly distribution to our unitholders.

- •

- Because of the natural decline in production from existing wells, our success depends, in part, on Antero's ability to

replace declining production and our ability to secure new sources of natural gas from Antero or third parties. Additionally, our fresh water distribution services are directly associated with

Antero's well completion activities and water needs, which are partially driven by horizontal lateral lengths and the number of completion stages per well. Any decrease in volumes of natural gas that

Antero produces, any decrease in the number of wells that Antero completes, or any decrease in the length of the laterals Antero drills, could adversely affect our business and operating

results.

- •

- We will be required to make substantial capital expenditures to increase our asset base. If we are unable to obtain needed

capital or financing on satisfactory terms, our ability to make cash distributions may be diminished or our financial leverage could increase.

Risks Inherent in an Investment in Us

- •

- Antero, our general partner and their respective affiliates, including Antero Investment, which will own our general

partner, have conflicts of interest with us and limited duties to us and our unitholders, and they may favor their own interests to the detriment of us and our other common unitholders.

- •

- Our partnership agreement replaces our general partner's fiduciary duties to holders of our units with contractual

standards governing its duties.

- •

- Holders of our common units have limited voting rights and are not entitled to elect our general partner or its directors,

which could reduce the price at which our common units will trade.

- •

- You will experience immediate dilution in tangible net book value of $ per common

unit.

- •

- There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may

not develop. The price of our common units may fluctuate significantly, which could cause you to lose all or part of your investment.

Tax Risks to Common Unitholders

- •

- Our tax treatment depends on our status as a partnership for federal income tax purposes, as well as us not being subject

to a material amount of entity-level taxation. If the IRS were to treat us as a corporation for federal income tax purposes, or if we become subject to entity-level taxation for state tax purposes,

our cash available for distribution to you would be substantially reduced.

Partnership Information

Our principal executive offices are located at 1625 17th Street, Denver, Colorado 80202, and our

telephone number is (303) 357-7310. Our website is located

at . We expect to make available

our periodic reports and other information filed with or furnished to the SEC free of

charge through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other

website is not incorporated by reference herein and does not constitute a part of this prospectus.

12

Table of Contents

The Offering

|

|

|

|

|

|

|

|

|

|

Common units offered to the public |

|

common units. |

|

|

|

common units if the underwriters exercise their option to purchase additional common units in full. |

|

Units outstanding after this offering |

|

common units

and subordinated units, for a total of limited partner

units. If and to the extent the underwriters exercise their option to purchase additional common units, we intend to use the net proceeds resulting from any issuance of common units upon such exercise to acquire an equivalent number of common units

from Antero, which common units would be cancelled. Accordingly, the exercise of the underwriters' option will not affect the total number of common units outstanding or the amount of cash needed to pay the minimum quarterly distribution on all

units. |

|

Use of proceeds |

|

We intend to use the anticipated net proceeds of approximately

$ million from this offering (based on an assumed initial offering price of $ per common unit, the mid-point

of the price range set forth on the cover page of this prospectus), after deducting the estimated underwriting discounts and offering expenses, to (i) repay in full $ million

of indebtedness that we will assume in connection with the contribution of Midstream Operating to us from Antero and (ii) reimburse Antero for $ million of capital

expenditures incurred in connection with the Predecessor prior to Midstream Operating being contributed to us. If and to the extent the underwriters exercise their option to purchase additional common units, we intend to use the net proceeds

resulting from any issuance of common units upon such exercise to acquire an equivalent number of common units from Antero, which common units would be cancelled. Accordingly, the exercise of the underwriters' option will not affect the total number

of common units outstanding or the amount of cash needed to pay the minimum quarterly distribution on all units. Please read "Use of Proceeds." |

|

|

|

Affiliates of certain of the underwriters are lenders under our Predecessor's existing midstream credit facility

and, accordingly, will receive a portion of the proceeds of this offering. Please read "Underwriting." |

|

13

Table of Contents

|

|

|

|

|

|

|

|

|

|

Cash distributions |

|

Within 60 days after the end of each quarter, beginning with the quarter

ending , 2014, we expect to make a minimum quarterly distribution of

$ per common unit and subordinated unit ($ per common unit and subordinated unit on an annualized basis) to

unitholders of record on the applicable record date. For the first quarter that we are publicly traded, we will pay a prorated distribution covering the period from the completion of this offering

through , 2014, based on the actual length of that period. |

|

|

|

The board of directors of our general partner will adopt a policy pursuant to which distributions for each quarter

will be paid to the extent we have sufficient cash after establishment of cash reserves and payment of fees and expenses, including payments to our general partner and its affiliates. Our ability to pay the minimum quarterly distribution is subject

to various restrictions and other factors described in more detail in "Our Cash Distribution Policy and Restrictions on Distributions." |

|

|

|

Our partnership agreement generally provides that we will distribute cash each quarter during the subordination

period in the following manner: |

|

|

|

• first, to the holders of common units,

until each common unit has received the minimum quarterly distribution of $ plus any arrearages from prior quarters; |

|

|

|

• second, to the holders of subordinated

units, until each subordinated unit has received the minimum quarterly distribution of $ ; and |

|

|

|

• third, to the holders of common units

and subordinated units pro rata until each has received a distribution of $ . |

|

|

|

If cash distributions to our unitholders exceed

$ per common unit and subordinated unit in any quarter, our unitholders and our general partner, as the holder of our incentive distribution rights ("IDRs"), will receive

distributions according to the following percentage allocations: |

|

|

|

|

|

Marginal Percentage

Interest in

Distributions |

|

|

|

Total Quarterly Distribution

Target Amount

|

|

Unitholders |

|

General Partner

(as holder of

IDRs) |

|

|

|

above $ up to $ |

|

|

85.0 |

% |

|

15.0 |

% |

|

|

above $ up to $ |

|

|

75.0 |

% |

|

25.0 |

% |

|

|

above $ |

|

|

50.0 |

% |

|

50.0 |

% |

|

|

We refer to the additional increasing distributions to our general partner as "incentive distributions." Please

read "How We Make Distributions to Our Partners—Incentive Distribution Rights." |

|

14

Table of Contents

|

|

|

|

|

|

|

|

|

|

|

|

We believe, based on our financial forecast and related assumptions included in "Our Cash Distribution Policy and Restrictions on

Distributions," that we will have sufficient cash available for distribution to pay the minimum quarterly distribution of $ on all of our common units and subordinated units for

the twelve-month period ending March 31, 2015. However, we do not have a legal or contractual obligation to pay quarterly distributions at the minimum quarterly distribution rate or at any other rate and there is no guarantee that we will pay

distributions to our unitholders in any quarter. Please read "Our Cash Distribution Policy and Restrictions on Distributions." |

|

Subordinated units |

|

Antero will initially own all of our subordinated units. The principal difference between our common units and

subordinated units is that, for any quarter during the subordination period, holders of the subordinated units will not be entitled to receive any distribution from operating surplus until the common units have received the minimum quarterly

distribution for such quarter plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. |

|

Conversion of subordinated units |

|

The subordination period will end on the first business day after we have earned and paid at least

$ (the minimum quarterly distribution on an annualized basis) on each outstanding common unit and subordinated unit for each of three consecutive, non-overlapping four-quarter

periods ending on or after , 2017 and there are no outstanding arrearages on our common units. |

|

|

|

Notwithstanding the foregoing, the subordination period will end on the first business day after we have earned and

paid at least $ (150.0% of the minimum quarterly distribution on an annualized basis) on each outstanding common and subordinated unit and the related distribution on the

incentive distribution rights, for any four-quarter period ending on or after , 2015 and there are no

outstanding arrearages on our common units. |

|

|

|

When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis,

and all common units will thereafter no longer be entitled to arrearages. |

|

Issuance of additional units |

|

Our partnership agreement authorizes us to issue an unlimited number of additional units without the approval of

our unitholders. Please read "Units Eligible for Future Sale" and "The Partnership Agreement—Issuance of Additional Interests." |

|

15

Table of Contents

|

|

|

|

|

|

|

|

|

|

Limited voting rights |

|

Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, our unitholders will have only

limited voting rights on matters affecting our business. Our unitholders will have no right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except for cause by a vote of the

holders of at least 662/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, Antero will own an aggregate

of % of our outstanding units (or % of our outstanding units, if the underwriters exercise their option to purchase additional common units in full). This

will give Antero the ability to prevent the removal of our general partner. In addition, any vote to remove our general partner during the subordination period must provide for the election of a successor general partner by the holders of a majority

of the common units and a majority of the subordinated units, voting as separate classes. This will provide Antero the ability to prevent the removal of our general partner. Please read "The Partnership Agreement—Voting Rights." |

|

Limited call right |

|

If at any time our general partner and its affiliates (including Antero) own more

than % of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price equal to the greater of (1) the average of

the daily closing price of the common units over the 20 trading days preceding the date three days before notice of exercise of the call right is first mailed and (2) the highest per-unit price paid by our general partner or any of its

affiliates for common units during the 90-day period preceding the date such notice is first mailed. If our general partner and its affiliates reduce their ownership percentage to below 70% of the outstanding units, the ownership threshold to

exercise the call right will be permanently reduced to 80%. Please read "The Partnership Agreement—Limited Call Right." |

|

Registration rights |

|

In connection with the completion of this offering, we intend to enter into a registration rights agreement with

Antero, pursuant to which we may be required to register the resale of common units, subordinated units or other partnership securities held by Antero. We may be required pursuant to the registration rights agreement and our partnership agreement to

undertake a future public or private offering and use the net proceeds to redeem an equal number of common units from Antero. In addition, our partnership agreement grants certain registration rights to our general partner and its affiliates. Please

read "Certain Relationships and Related Transactions—Agreements with Affiliates in Connection with the Transactions—Registration Rights Agreement" and "The Partnership Agreement—Registration Rights." |

|

16

Table of Contents

|

|

|

|

|

|

|

|

|

|

Estimated ratio of taxable income to distributions |

|

We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period

ending , , you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be less

than % of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $ per unit,

we estimate that your average allocable federal taxable income per year will be no more than approximately $ per unit. Thereafter, the ratio of allocable taxable income to cash

distributions to you could substantially increase. Please read "Material U.S. Federal Income Tax Consequences—Tax Consequences of Unit Ownership" for the basis of this estimate. |

|

Material federal income tax consequences |

|

For a discussion of the material federal income tax consequences that may be relevant to prospective unitholders

who are individual citizens or residents of the United States, please read "Material U.S. Federal Income Tax Consequences." |

|

Exchange listing |

|

We have applied to list our common units on the New York Stock Exchange (the "NYSE") under the symbol

"AM." |

|

17

Table of Contents

Summary Historical and Pro Forma Financial and Operating Data

We were formed in September 2013 and do not have historical financial statements. Therefore, in this prospectus we present the

historical financial statements of our Predecessor. The following table presents summary historical financial data of our Predecessor as of the dates and for the periods indicated.

This prospectus includes audited financial statements of our Predecessor as of and for the years ended December 31, 2011, 2012 and 2013. This prospectus also includes summary pro

forma financial data as of and for the year ended December 31, 2013. For a detailed discussion of the summary historical financial information contained in the following table, please read

"Management's Discussion and Analysis of Financial Condition and Results of Operations." The following table should also be read in conjunction with "Use of Proceeds" and the audited historical

financial statements of the Predecessor included elsewhere in this prospectus. Among other things, the historical financial statements include more detailed information regarding the basis of

presentation for the information in the following table.